Real Estate

An overview of one of India's promising sectors with 2 companies analyzed.

India’s real estate sector has quietly transformed over the past decade, from a trust-deficit industry plagued by delays and opacity, to one witnessing consolidation, regulatory reform, and rising formalization. As housing demand surges and listed developers gain market share, it's worth stepping back to understand the structural and cyclical forces shaping this evolution.

Where is this industry headed?

The love for owning properties is increasing substantially, especially among high-net-worth individuals (HNIs) in India. India’s HNI and Ultra HNIs are expanding at around 11% annually, leading to the demand for premium properties to outpace the affordable ones.

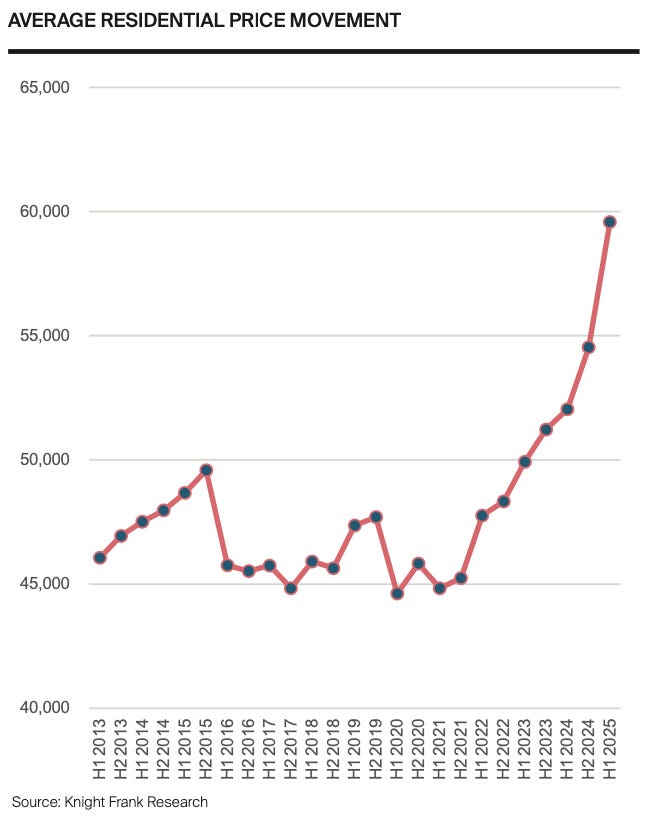

We’re seeing rapid price hikes in several key cities, like Ahmedabad, Banglore and the NCR.

This industry has a promising future, and is equipped with both volume and value expansion.

In fact, the highest percentage real estate contributed to India’s total market cap was ~6% in 2008. It made a new low in 2020 at ~1.5%. It’s currently at ~2%. If we use a simple mean reversion mental model, I believe we can safely predict the contribution to correct to roughly 4%. Lots of growth ahead!

Cyclical Nature

The real estate sector is known to have extremely long-dated cycles, some known to last for decades. I believe Ishmohit Arora from SOIC explains the cyclical nature of the industry best, in 4 stages:

The prospect of high returns leads investors to become increasingly optimistic

Increasing competition causes returns to fall below the cost of capital, causing stocks to underperform

Reduced business investment leads to greater industry consolidation as more firms exit. Investors become pessimistic.

Improvements in the supply side cause returns to rise above the cost of capital, causing stocks to now outperform

Since this is a highly cyclical sector, it’s important to track the debt and unsold inventory of a company as it can be dangerous during the downtrend

How Real Estate Businesses Work

There are three main sources of revenue for Real Estate companies:

Construction based: Development of property

Rental Based: Rent, office leases

Hotels, exhibitions etc.

There are several ways to finance projects as well:

Land Bank Model, where they own the land itself and construct from there

Joint Development Model (JDM), where there is a partnership between a landlord and a developer where the topline is shared with the landowner, but costs and development are undertaken by the developer

Independent Contractor Model, where a developer is hired purely as a contractor to build the project, typically for a fixed fee or cost-plus margin

Accounting & Terminology

Real estate companies follow the project delivery method for accounting. Typically, we know that revenues are booked when goods are shipped. But in this case, a company can only book revenues when a project is completed and delivered to the buyer. However, they must book marketing and business development costs as they go.

This is why following the P/L statement can be tricky and misleading

Area Booked: The total area booked by customers while purchasing property

Realization: How much revenue the company is earning per square feet

Pre-sales: The initial commitment made by customers to the developer

Collection: Total money collected against total area booked

Advances: Total amount collected for property under development which has not yet been realized as revenue

Rental Yield: Rent received annually

Valuation

As mentioned before, I would avoid using the P/L statement to value companies as we might do for others. Instead, pay attention to business development and the value of a company’s planned projects, the average completion time, collection efficiency.

A sum-of-the-parts model might be suitable for real estate companies that have both rental and construction income:

For the rental portion, you can apply ~15x PE. This will be higher than the construction side as rental income is highly predictable

For the construction portion, you can use MC/Pre-sales and give it a 3-4x multiple. Personally, I feel like this would lead to uncomfortably high valuations, so I prefer using EV/EBITDA. For the mid-cap range, I’ve found a conservative estimate to be around 10x

Remember, it’s always better to be conservative in your valuations than aggressive. Any surprise can only lead to further upside!

Arvind Smartspaces & Max Estates

I believe both are very interesting companies who are well positioned to capitalize on the real estate theme.

Disclaimer: No buy or sell recommendations, please do your own due diligence.

Arvind Smartspaces

This is the real estate arm of the Lalbhai Group (valued at ~$2bn). They develop projects either through owned land or the JDM model. They design and build spaces and categorize their projects are either horizontal (towns, villas), or vertical (buildings). Horizontal accounts for roughly 80% of the portfolio, leaving vertical with 20%. They’re focused on residential projects, primarily in Ahmedabad and Bengluru but expanding into Pune, Surat and Mumbai as well. They mainly cater to the mid market (>80%), and have a small exposure to luxury projects as well.

The main growth driver here is their expansion into new geographies, whilst maintaining their strong pricing power (20-25% up in Ahmedabad) in key cities. Their projects are constantly being fully sold at launch, and the management is highly optimistic and confident that they can deliver operational excellence during aggressive expansion (they have mentioned plans to improve execution as per recent concalls)

My valuation thinking:

They are targeting 6-7 acquisitions in FY26 with a cumulative topline potential of 4000-5000cr.

4000 topline * 25% EBITDA * 10x EV/EBITDA multiple = 10,000 cr EV

Even assuming 1000 cr of debt, we’re still left with an equity value of 9000 cr. Assuming these projects will be delivered by 5 years, this could be value in 2030. The current market cap is around 3000 cr.

Also, the management is expecting ~4000 cr of net operating cashflow in a few years. This is 25% more than the current market cap, and we haven’t even factored in the terminal value yet.

Max Estates

This is part of the Max Group, another gold-plated group known to nurture strong companies in the past. They have a strategic partnership with New York Life, who have committed more than 1000 cr. Max is focused on Delhi, Noida and Guragon, but they’re actively studying tier 2 NCR markets as well. Unlike Arvind, Max has more exposure to commercial projects as well. Here is their roughl breakup: Commercial (24%), Residential (46%),Mixed (30%). They have big names as their tenants, such as BBC, Axis Bank, Tata, Samsung etc.

I think Max has a good opportunity to capitalize on rising premium segment, and also command very high pricing premiums in their key cities (40% on their “Phase 2” project). They have also mentioned plans on heavy capex in the coming years.

My valuation thinking:

They have guided for 25,500 cr presales in total by FY28.

25500 * 25% EBITDA / 4 = 1600 average EBITDA * 10 EV/EBITDA multiple = 16,000 cr EV.

They are also guiding for 723 cr rental income in 5 years. Applying a 15x PE makes it 10,800 cr.

Adding the two together, we get 26,800 cr EV in 5 years. Assuming even 2000 cr of debt leaves us with almost 25,000 cr of Market Cap by 2030.

Also, if you get a chance, check out the renders on their planned projects (found on investor presentations). You’ll see they’re extremely high in quality and resemble some of the finest neighborhoods you find in Dubai!

Risks

Both companies have highlighted potential risks in a consolidation of market demand for real estate, and have mentioned possible increases in land prices.

A significant portion of this article has to be credited to the work of Ishmohit Arora from SOIC. I’ve also used research from Knight Frank.