Caplin Point Laboratories

30 Years of boring compounding in plain sight

Explaining Caplin

Caplin Point Laboratories makes generic medicines and sells them across 23 countries, with the bulk of its revenue coming from Latin America. The company was founded in Chennai in 1990 as a contract manufacturer, meaning it made medicines for other companies under their labels. Over the following three decades, it evolved into a business that owns its own brands, controls its own distribution infrastructure in foreign markets, and manufactures complex pharmaceutical products for both emerging and regulated markets.

Latin America and Francophone Africa

This is where Caplin built its franchise. Latin America accounts for 76% of revenue, Africa for 3%.

Caplin has established legal subsidiaries in individual countries across Central and South America, including Guatemala, Nicaragua, Honduras, El Salvador, Ecuador, Colombia, Chile, and Mexico. It holds inventory in-country, registers its own products with local drug regulators, and supplies pharmacies and hospitals through its own distribution relationships. The company has over 22,000 distribution touchpoints across the region.

Because Caplin controls the supply chain down to the pharmacy level, its customers in these markets pay quickly, often in advance. This produces a structurally negative working capital cycle, which is rare for a manufacturing business of this kind.

The product mix in these markets is 75% generic and 25% branded generic. A branded generic is a generic drug sold under a company’s own brand name, which allows for a price premium over unbranded alternatives. The branded generic share has grown from just 5% in FY2012, and that shift is what drives the gross margin profile. Across 36 therapeutic segments, the portfolio covers over 65% of the WHO essential drug list.

United States (through Caplin Steriles)

The US business contributes 21% of revenue and operates through Caplin Steriles Limited, a subsidiary with a USFDA-approved injectable manufacturing facility at Gummidipoondi, Chennai.

Injectables are more complex to manufacture than oral tablets. They must be sterile, and the facility must pass regular USFDA inspections to remain eligible to supply the US market. Caplin Steriles has cleared four consecutive inspections with clean outcomes.

The US business currently runs on two models: supplying other American pharmaceutical companies under their labels (B2B, 75% of CSL revenue) and selling under Caplin’s own label through Caplin Steriles USA Inc, its American front-end entity (B2C, 25%). As of FY26, Caplin holds 59 ANDA approvals, each representing regulatory clearance to sell a specific generic drug in the US. The front-end entity achieved profitability in its first year of operations.

Theme

Latin America: The Market Nobody Wanted

Let’s start with geography, because that is where the story begins.

Latin America has a combined population of roughly 660 million people. Per capita incomes across most of the region sit well below OECD levels. The average patient in Guatemala, Honduras, or Ecuador cannot pay Rs. 1,500 for a branded drug. But they still get diabetes, hypertension, and bacterial infections that need antibiotics and parasitic infections that need dewormers. Generic pharmaceuticals in these markets are the only realistic option.

The Latin American pharma market is approximately $75 billion today and is expected to reach $102 billion by 2030. Generics account for 62% of that market. The generics sub-segment grows faster than the overall market because governments across the region have spent the past two decades passing legislation that actively promotes generic adoption to reduce public healthcare spending. Brazil passed its landmark generic medicines law in 1999, Mexico has progressively mandated that pharmacists offer a generic substitute for any branded prescription, Colombia has similar substitution policies.

Also, Latin America is urbanizing rapidly. As populations shift from rural subsistence into urban wage employment, healthcare utilization through formal pharmacy channels rises. This is the patient who walks into a pharmacy, asks for a medicine by name, and buys it every month for years. Chronic disease medications for hypertension, diabetes, cardiovascular conditions, and respiratory illness are repeat-purchase, high-frequency products. This is the best possible kind of demand for a pharmaceutical company.

What makes Caplin’s position unusual is that it has been building this market presence since 1994. When Caplin entered Angola and then Central America, no significant Indian pharmaceutical company was paying attention to the region. The regulatory complexity was seen as too difficult, markets were seen as too small, not to mention the currency and political risk. Caplin went anyway, registered its products country by country, built relationships with distributors and pharmacies, put its own brand names on medicines, and compounded those relationships over three decades.

The result today is a business with product registrations across 23 countries, over 5,000 product licences across 36 therapeutic areas, distribution reach covering tens of thousands of pharmacy touch points, and brand recognition that took twenty years to build. A competitor entering LatAm today would face the same queue Caplin faced in 1995, except Caplin has already crossed the finish line and the competitor is still at the starting blocks.

The financial proof of this market position is Caplin’s working capital structure. In most generic pharma supply relationships, the supplier ships goods, extends credit, waits 60 to 90 days, and hopes collections come in. Caplin’s LatAm distributors pay in advance or on very short credit terms. This happens because Caplin controls the shelf. If you are a distributor in El Salvador and Caplin is your most reliable supplier of antibiotics, antifungals, and antihypertensives across twenty therapeutic categories, you do not make them wait for payment. The consequence is that Caplin’s LatAm business operates with a structurally negative working capital cycle. This is a rare thing in manufacturing and an almost unheard of thing in emerging market pharma exports.

The United States: The Right Door into a Complex Market

Most Indian pharmaceutical companies that tried to build a meaningful US business went through the oral generics market first (tablets, capsules, oral liquids). It seemed like the natural starting point because the manufacturing was simpler and the regulatory pathway was well understood. What happened was predictable in hindsight. When a branded drug patent expires and a generic tablet is approved, the first few manufacturers earn strong margins. Then more manufacturers get approved, prices collapse 80 to 90% within two to three years, and the entire segment becomes a commodity with thin margins and brutal price competition. Dozens of Indian companies have spent the past decade writing down goodwill from US generic acquisitions and watching their US margins compress quarter after quarter.

Caplin watched this happen and went through a different door entirely: Sterile injectable manufacturing.

Injectable drugs delivered intravenously or intramuscularly are technically far harder to produce than oral solids. The manufacturing facility must meet extremely stringent contamination control standards. Cleanrooms classified to ISO specifications, aseptic fill-finish lines, and overall a rigorous monitoring environment. The capital investment required runs into hundreds of crores and the technical expertise is genuinely scarce. This means that when a drug requiring an injectable form goes off-patent, far fewer manufacturers can produce a generic version compared to a tablet. Competition is thinner. Prices hold up better. Margins are structurally higher.

The US generic sterile injectable market is approximately $18 billion today, growing toward $43 billion by 2035 at a 9.2% annual growth rate. This growth is driven by a large and ongoing wave of branded drug patent expiries, many of which involve injectable formulations. Every patent expiry creates a new ANDA opportunity. Caplin Steriles has 59 approved ANDAs today, with 55 more in the development pipeline for filing over the next four years.

Within the injectable category, Caplin has made a specific product selection choice that is worth understanding. The company has deliberately prioritized pre-filled syringes, ophthalmic products, and Blow-Fill-Seal technology for its pipeline. These are the most technically demanding forms in the injectable category, and they have the fewest qualified manufacturers competing for market share.

There is also a structural demand dynamic that helps new qualified entrants. The US FDA maintains a public drug shortage list at any given time containing roughly 100 to 200 drugs, the majority of which are generic sterile injectables. Shortages occur when a manufacturer has a quality event and must suspend production, or when demand spikes faster than capacity can respond. The FDA has created expedited review pathways for ANDAs addressing drugs in shortage. For Caplin, a USFDA-compliant injectable manufacturer, these shortages represent a recurring, self-replenishing set of opportunities to enter segments where the competitive field has temporarily narrowed.

GLP-1 Generics Optionality

GLP-1 receptor agonists are a class of drugs that have gone from a diabetes treatment to a cultural phenomenon in the span of five years. Drugs like Ozempic and Wegovy have demonstrated dramatic weight loss results in clinical trials and have become among the best-selling pharmaceuticals in history. The US GLP-1 market reached $71 billion in 2024. The global market is projected to exceed $100 billion by 2030.

The branded versions cost upwards of $1,000 per month in the United States. In Latin America, they are essentially inaccessible for the vast majority of patients.

This is where the Caplin angle becomes interesting. Liraglutide, one of the first major GLP-1 drugs, had its primary US patents expire in late 2023, and generic versions entered the US market in late 2024. The timeline for semaglutide generics is longer and more complex due to Novo Nordisk’s patent portfolio, but the direction of travel is clear.

The reason this matters specifically for Caplin comes down to geography and manufacturing capability.

Latin America has some of the highest rates of diabetes and obesity in the world, and it’s disproportionate relative to their income levels. The patient population that would benefit most from GLP-1 drugs is concentrated precisely in the markets where Caplin has its deepest distribution infrastructure. A generic liraglutide or semaglutide at 1/10th the branded price, supplied by a company that already sits on pharmacy shelves across Guatemala, Honduras, El Salvador, Ecuador, and Colombia, is a fundamentally different commercial proposition than the same generic drug trying to build a distribution network from scratch.

On the manufacturing side, GLP-1 drugs are subcutaneous injectables delivered by pre-filled pen devices. Caplin’s injectable manufacturing capability is directly applicable. The company has stated in its Q4 FY26 earnings presentation that it awaits regulatory approvals from Central American countries for its own internally developed GLP-1 products, with plans to expand to other South American markets post-patent expiry in FY28.

Oncology: Institutional Channel Advantage

Cancer is among the fastest-growing disease burdens in Latin America. The World Health Organization projects that Latin America will see a 65% increase in cancer incidence by 2040, driven by aging populations, urbanization, and changing lifestyle patterns. Governments across the region are expanding public healthcare coverage for cancer treatment as political pressure from patient advocacy groups intensifies.

Oncology drugs are overwhelmingly dispensed through institutional channels, meaning hospitals, oncology clinics, and government health programmes, rather than retail pharmacies. This is exactly the channel that Caplin has been building in Latin America through its institutional sales program, which already accounts for 20% of its emerging markets revenue.

A company that already has established relationships with hospital procurement departments and government health ministries across 23 countries has a significant advantage when it moves into oncology.

Caplin’s oncology facility at SIDCO Kakkalur, near Chennai, has completed its first regulatory inspection successfully. The company has acquired several oncology ANDAs from third parties. A separate Oncology API facility at Thervoy SIPCOT is under construction, with first Drug Master File filings targeted for FY28. The backward integration into oncology APIs means Caplin would eventually control the full stack from the active ingredient through to the finished drug, which is the same cost structure advantage it has been building in general APIs for its existing portfolio.

Oncology is a long-duration build. The therapy area requires careful regulatory navigation, specialised manufacturing protocols, and deep clinical relationships.

Africa: The LatAm Story, 30 Years Earlier

Africa contributes approximately 3% of Caplin’s revenue today. That number invites dismissal, but let’s review a previous pattern.

In 1994, Caplin entered Angola with a Stock and Sale model when Latin America was widely considered too difficult, too fragmented, and too risky to justify serious investment. Thirty years later, Latin America is 76% of the company’s revenue and the foundation of its compounding machine. Africa today sits in a similar position to where LatAm was in 1994.

The African pharmaceutical market is approximately $27 billion, growing toward $37 billion by 2033. Roughly 60% of medicines consumed across the continent are imported, primarily from India and China. Local manufacturing capacity is grossly insufficient relative to the population and regulatory frameworks are fragmented on a country-by-country basis, which serves as a barrier to entry for any company unwilling to do the country-level regulatory work systematically over many years. Distribution infrastructure is underdeveloped and healthcare spending per capita is rising but from a very low base.

Every one of those characteristics describes Latin America in the mid-1990s. Caplin navigated that environment and built a near-monopoly position. The playbook is proven, and the question is whether management has the patience and institutional capability to replicate it in a new geography over a similar timeframe.

The African Continental Free Trade Agreement adds a potential structural catalyst. Signed by 54 of 55 African Union member states, it is progressively working to reduce intra-African trade barriers. For a pharmaceutical company that has invested in country-level regulatory approvals across multiple African markets, a future where a product registered in one country can be sold across a broader trade zone would multiply the value of those registrations significantly.

The Structural Shift in Generic Pharma: Complexity Wins

There is a broader industry transition underway that provides the backdrop for everything Caplin is building in the US.

The era of straightforward generic pharmaceuticals, simple tablets and capsules competing primarily on price, is largely over for Indian companies in developed markets. The returns from oral solid generics in the US have been competed away. Companies that built large businesses around generic tablet manufacturing in the 2000s and 2010s have spent the past several years watching margins compress and writing down acquisitions made at the peak of that cycle.

The next decade of opportunity in generic pharmaceuticals sits in technical complexity. These products require significant technical investment, take longer to develop and manufacture, and attract fewer qualified competitors. Caplin entered the US through injectables from the beginning, precisely because the oral generics path was already showing signs of deteriorating economics.

The China plus one dynamic accelerates this transition. COVID-19 exposed how concentrated pharmaceutical supply chains had become around Chinese API manufacturers. Approximately 70% of active pharmaceutical ingredients consumed globally come from China, so when Chinese API production was disrupted, the downstream effects on drug availability in hospitals across the United States were immediate and severe. Post-COVID, both US government procurement policy and private hospital procurement behaviour have shifted toward qualifying alternative suppliers, specifically non-Chinese sources, for critical pharmaceutical ingredients.

Caplin is building its own API manufacturing capability as a direct response to this environment. The Vizag API facility has received its manufacturing licence and completed validations for several APIs already. The company has completed research and development for over 90 APIs intended for backward integration into both its US injectable pipeline and its existing LatAm portfolio. As this backward integration completes, Caplin’s supply chain becomes simultaneously less expensive, more resilient, and better positioned to meet the sourcing standards that US hospital procurement is increasingly demanding.

The China 2.0 strategy adds another dimension to this. Rather than developing all new products from scratch, Caplin has established partnerships with Chinese pharmaceutical companies that already hold approved ANDAs or marketing authorizations in the US and EU. Caplin then files those same products in its LatAm markets, accessing a broader product range faster than its own R&D pipeline could supply, and paying for proven product development rather than uncertain early-stage research. The first biosimilar product filing in Central America came through this program.

Value

Caplin’s EBITDA margin in FY26 was 38%. The Indian pharma sector average sits between 18% and 22%. Branded domestic pharma companies, which sell under their own names to Indian doctors and pharmacies, typically run 22 to 26%. Caplin, a generic pharmaceutical exporter selling primarily into Latin America and the US, runs 38%.

Why the Margins Are This High

Most consumer-facing pharmaceutical companies spend 25 to 35% of revenue on selling, marketing, and distribution. Caplin’s LatAm business is institutional and wholesale-led. It sells to established distributors who already reach the pharmacies. There is no advertising spend, so the operating cost structure is fundamentally leaner than a consumer pharma model.

Vertical integration: Caplin manufactures approximately 60% of its products in-house and has progressively built its own API manufacturing capability. Gross margins in FY26 were 60.4%, expanding from approximately 50% in FY17.

The Negative Working Capital Model

Working capital is the money a business needs to bridge the gap between paying its suppliers and receiving payment from its customers. A company with 90-day receivables needs to finance three months of its own revenue. This costs money, either through bank borrowings or by tying up internal cash.

Caplin’s LatAm business runs with a structurally negative working capital cycle.

Estimated receivable days in its core markets are approximately 8 to 12 days. Distributors in Guatemala, Honduras, Ecuador, and Colombia pay Caplin within days of receiving goods, because Caplin is often the most reliable supplier of quality generic medicines across twenty therapeutic categories in their market.

This means Caplin’s LatAm operations are funded by their own customers. Cash comes in before it goes out. The business does not need bank facilities to manage its working capital. This is the financial proof of market power, and it happens automatically when a business controls the relationship.

ROCE Through a Capex Cycle

Return on Capital Employed has stayed above 25% for five consecutive years. The Indian pharma sector average is 12 to 18%.

The more revealing number is that this ROCE was maintained through the injectable facility construction cycle of FY20 to FY22, when Caplin was deploying approximately Rs. 650 crore into a new USFDA-compliant manufacturing plant at Gummidipoondi. Most companies see ROCE compress sharply during heavy capex because capital is being deployed before it earns revenue. Caplin’s ROCE floor during this period was approximately 25%. That tells you the underlying LatAm business was generating returns so far above 25% that the idle capital drag of a half-built facility could not pull the blended rate below the threshold.

The injectable facility is now substantially complete. As US injectable revenue scales through this already-depreciated asset base, each new rupee of US revenue flows at very high incremental ROCE. This is the margin expansion catalyst that has not yet appeared in the numbers.

The Balance Sheet

Finance costs in FY26 were Rs. 0.87 crore. On Rs. 650 crore of PAT, that is 0.13% of annual profit going to interest. Caplin has never borrowed meaningfully in 35 years of operations. The injectable facility, the US front-end, the oncology facility, and the API plants are all being built from what the business generates.

The zero-debt balance sheet eliminates constraints on management decision-making entirely. When Caplin acquired 10 ANDAs in January 2026 targeting a $473 million US market, it was funded quietly from cash with no equity dilution and no press release about raising capital.

Operating Leverage: The Compounding Effect

EBITDA margin was approximately 21% in FY14. It is 38.1% today. Revenue has grown roughly 12 times over that period.

There is more runway. The US injectable facility is a fixed cost base currently earning modest revenue. As the ANDA portfolio matures and US front-end revenue scales, each new rupee of US revenue uses infrastructure whose costs are already absorbed. The operating leverage from the US business has not yet appeared in the consolidated margins. When it does, the progression from 38% to something above it will be a function of scale rather than any change in the underlying business.

Growth

Latin America

The bear case on LatAm has always been saturation, but the evidence says otherwise. Caplin products occupy 41% of shelf space across independent pharmacies in Central America. The company’s stated target is 57%, achievable by adding a liquid manufacturing facility to register categories currently missing from the portfolio.

A business with 41% shelf space in its core markets, with a clear product-led path to 57%, is nowhere near saturation. It is mid-penetration in markets it has operated in for over twenty years.

Mexico and Chile are the newer engines. Mexico has 25 product registrations so far, with over 120 more to be filed in the next 18 months from the combined pipelines of Caplin Point, Caplin One Labs, and Caplin Steriles. The company has won 11 general and oncology products for tender supply in Mexico worth approximately $4 million over the next 24 months. More importantly, Caplin has purchased land to build its first local manufacturing facility in Mexico, which unlocks a 16% price advantage in government tenders once local production begins. In Chile, 135 product registrations are in place, $10 million of tender wins have been secured for the next 24 months, and management is actively evaluating two distribution company acquisitions to reach the private pharmacy market more directly.

Brand marketing is the next layer on top of distribution depth. Caplin is entering CNS therapy as a branded marketing play in Dominican Republic, Guatemala, and Nicaragua, with bioequivalence already completed for over 12 products and commercial launches planned for September 2026. This is the shift from selling generics through a wholesale channel to building prescription demand at the doctor and pharmacist level. The margin implication of that shift, as the branded generic share moves from 25% toward 35% of LatAm revenue, is significant.

United States

Caplin Steriles Limited generated Rs. 470 crore in FY26 revenue at a 30% EBITDA margin for the full year, expanding to 33% in Q4 alone. Caplin Steriles USA, the front-end commercial entity, completed its first full year of operations with $11 million in revenue and a 26.2% EBITDA margin.

Caplin went into the US through pre-filled syringes, ophthalmics, and IV bags rather than the commodity vial segments where margins erode quickly. The product quality is also visible in per-ANDA revenue: Vivek Partheeban noted on the concall that Caplin’s average revenue per ANDA is more than 50% above the industry average of $800,000 to $1 million.

There is a more important point buried in the breakdown. Of the US growth Caplin delivered in FY26, over 90% came from products that were already launched before the year began. The 10 ANDAs approved during FY26 and the 15 ANDAs acquired in January 2026 have mostly not yet been launched commercially. The largest ones are in the process of being launched over the coming weeks. Management guided 25% to 30% growth for the overall Caplin Steriles business in FY27, and separately set a target of doubling the Caplin Steriles USA own-label revenue from Rs. 100 crore to Rs. 200 crore. Both targets will be driven substantially by products already approved but not yet generating revenue.

The capacity picture makes the next three years even clearer. Today, Caplin Steriles operates with five injectable lines (three older lines and two new ones). The Phase III expansion will bring the total to 17 injectable lines within two to three years. The COL-II facility at Gummidipoondi is completing by December 2026 and will house five additional lines for injectables, ophthalmics, and Blow-Fill-Seal products. Caplin is simultaneously moving high-volume, lower-margin injectable products to compliant contract manufacturers, freeing existing in-house lines for higher-margin complex products.

The non-US regulated market piece is often overlooked entirely. Caplin Steriles has filed 54 products across Canada, EU, Australia, Mexico, Brazil, South Africa, Saudi Arabia, and UAE, of which 32 are approved. Management expects meaningful revenue from these markets in FY27. This is a third revenue stream within the US business.

What Hasn’t Started Yet

The oncology facility completed its first regulatory inspection successfully and has been capitalized post April 2026. The Thervoy oncology API facility is completing by Q3 FY27 with first Drug Master File filings planned for FY28. Oncology products will flow through distribution relationships with hospital channels that Caplin has spent twenty years building in LatAm.

The GLP-1 pipeline is the one that nobody is talking about. Caplin awaits regulatory approvals from Central American countries for internally developed GLP-1 products, with plans to expand to other South American markets post patent expiry in FY28. The combination of an injectable manufacturing capability, an existing distribution network reaching diabetic and obese patient populations across Latin America, and a generic GLP-1 at 1/10th the branded price creates an opportunity that has no precedent in Caplin’s history.

The China 2.0 strategy continues to build. Multiple partnerships with Chinese companies holding approved ANDAs or marketing authorizations in the US and EU have generated filings across Mexico, Colombia, and Chile, plus the first biosimilar product filing in Central America. This expands the product range at a fraction of the cost of in-house development and brings biologics into a company that has historically been a small-molecule generics manufacturer.

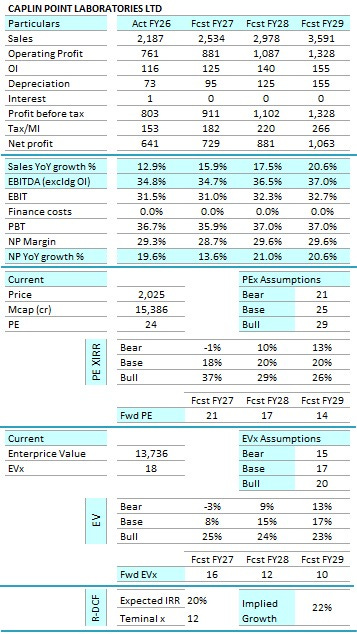

Valuation

Disclaimer: This is not investment advice. I am not a SEBI-registered analyst. Please do your own research before making any investment decisions.